Loan Origination System (LOS): Complete Guide for Banks & NBFCs

Digital lending has transformed how banks and NBFCs operate. Loan applications are now submitted through mobile apps, web portals, APIs, and partner ecosystems. Credit reports are fetched instantly. Sanction letters are generated digitally.

Yet many institutions discover an uncomfortable truth:

“Going digital does not automatically mean being structured.”

Many financial institutions realize their applications are still get stuck in underwriting queues. Credit policies are applied inconsistently. Compliance documentation requires manual validation. Risk assessments vary across branches. Audit trails are reconstructed retrospectively.

But structured lending requires orchestration. That orchestration is delivered by a Loan Origination System (LOS).

This guide explains the ins-and-outs of loan origination and how a los system effectively addresses the gaps enterprises experience today.

What is a Loan Origination System?

A Loan Origination System (LOS) is a centralized software platform that automates, structures, and governs the entire pre-disbursement process of lending, including:

- Loan application capture

- KYC verification

- Credit bureau integration

- Risk assessment automation

- Underwriting workflow

- Rule-based decision engine

- Documentation management

- Compliance validation

- Approval routing

- Disbursement triggers

It replaces manual, email-driven, spreadsheet-based loan processing with workflow automation and policy enforcement.

Why Loan Origination Systems Matter in the Indian Banking Sector?

In India, banks and NBFCs operate under strict oversight from the Reserve Bank of India (RBI). Regulatory frameworks include:

- RBI Digital Lending Guidelines

- KYC norms under PMLA

- Fair lending practices

- Audit and reporting mandates

Institutions must maintain:

- Transparent approval hierarchies

- Complete audit trails

- Standardized risk policies

- Data protection safeguards

But here’s the thing. Manual or semi-digital systems struggle to meet these expectations at scale. This is where a Cloud-based loan origination platform can help. A cloud-based LOS embeds compliance straight into workflows, enabling strict oversight. And since compliance becomes systematic, you’re essentially reactive not waiting for dangers to happen.

For instance, having an automated LOS with compliance workflows enables the following scenarios:

- If KYC documentation is incomplete → workflow cannot proceed.

- If credit score falls below threshold → automated decline or escalation.

- If policy exception occurs → mandatory senior approval triggered.

How a Loan Origination System Works (End-to-End Workflow)

When a customer applies for a loan today, they expect speed. They expect clarity. And most importantly, they expect a smooth experience — whether they apply from a branch, a website, or a mobile app.

Behind the scenes, a Loan Origination System (LOS) ensures that this journey feels seamless. Let’s walk through how it works in real-world terms.

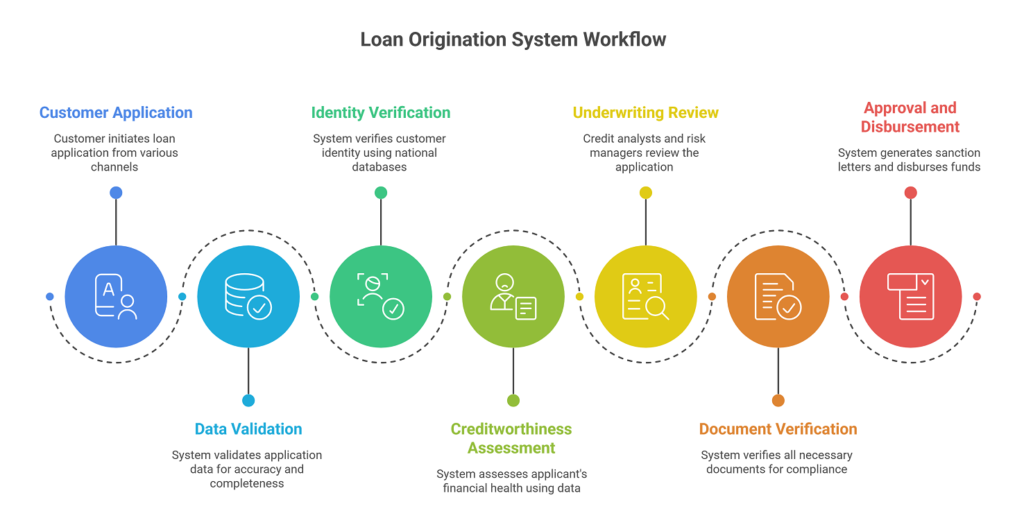

1. Multi-channel Application Intake

A loan journey can begin anywhere.

Some customers walk into a branch. Others apply through an online portal. Many prefer mobile apps. In some cases, fintech partners or third-party platforms send applications through APIs.

A modern LOS brings all these entry points into one unified system. No matter where the application starts, it lands in a single structured environment.

The system validates information instantly — checking if required fields are filled, verifying formats, and even detecting duplicate applications. This prevents errors and fraud at the very first step.

Instead of messy data flowing into operations, the organization starts with clean, verified information.

2. Identity and KYC Are Verified in Real Time

Once the application is captured, the next critical step is identity verification.

Earlier, this process required physical documents, manual checks, and multiple follow-ups. Today, the system connects directly to national identity databases and compliance systems.

PAN and Aadhaar details are validated instantly. AML (Anti-Money Laundering) screening runs automatically. Fraud detection engines scan for suspicious patterns. Credit bureau systems such as CIBIL, Experian, or CRIF are accessed in real time.

What used to take days can now happen in minutes.

The result? Faster onboarding without compromising regulatory compliance.

3. Creditworthiness Is Assessed Using Data, Not Guesswork

After identity verification, the system evaluates the applicant’s financial health.

It retrieves credit bureau data, calculates debt-to-income ratios, and applies internal credit policies. Applications are categorized into risk bands based on predefined rules.

In more advanced setups, AI-powered underwriting models analyze behavior patterns, spending habits, and anomalies to refine risk assessment.

This ensures decisions are consistent and policy-driven — not dependent on individual judgment alone.

For the customer, this means quicker decisions.

For the institution, it means controlled risk exposure.

4. Risk Analytics and Real-Time Dashboards

Operational visibility is essential for leadership teams.

A modern LOS provides dynamic dashboards that track key performance indicators such as loan approval ratios, average turnaround time (TAT), portfolio segmentation, underwriting productivity, and emerging fraud signals.

These insights allow management to identify bottlenecks, adjust credit policies proactively, and monitor portfolio health in real time.

Instead of relying on static reports generated at month-end, decision-makers gain continuous visibility into lending performance.

5. Embedded Compliance and Enterprise-Grade Security

Financial institutions operate in a tightly regulated environment. Compliance cannot be treated as an afterthought.

Enterprise-grade loan origination software embeds security and governance directly into the platform. Sensitive borrower data is protected through strong encryption standards. Role-based access controls ensure that employees view only what they are authorized to see. Every action taken within the system is recorded through detailed audit trails.

Regulatory reporting requirements can be supported through structured data capture and traceable workflows.

Beyond regulatory adherence, strong data governance controls protect institutional reputation and customer trust.

Security and compliance are not additional modules — they are built into the core architecture.

Key Features of Modern Loan Origination Software

When you evaluate a Loan Origination System, you are not just selecting software. You are choosing the operational backbone of your lending business.

The right system should not force you to change your processes. It should strengthen them, standardize them, and give you better control as you scale.

Here’s what you should expect from a modern, enterprise-ready LOS.

1. Workflow Automation That Mirrors Your Lending Structure

Your lending products are different and your workflows should reflect that.

Retail personal loans move differently from SME lending. Corporate credit requires layered approvals. Housing finance demands document-heavy verification. Microfinance operations depend on speed and volume.

Your LOS should allow you to configure workflows specific to each product line. Approval hierarchies, credit checkpoints, escalation paths, everything should be adaptable.

With low-code configuration, you should be able to update credit policies, change approval rules, or introduce new lending products without long development cycles.

Remember, if your policies change, your system should adjust with you, not slow you down.

2. A Rule Engine That Protects Credit Discipline

Underwriting consistency is critical for any lender.

A built-in rule and decision engine ensures eligibility validation, risk scoring, and pricing logic follow defined policies — not individual interpretation.

When exceptions arise, the system should automatically escalate them to the right authority. When applications meet predefined criteria, they should move forward without delay. This reduces subjectivity, improves turnaround time, and strengthens risk governance.

For you, this means faster approvals without compromising credit quality.

3. API-Based Architecture That Eliminates Silos

Your Loan Origination System should not operate in isolation.

It must connect seamlessly with your Core Banking System, CRM platform, payment gateways, fraud detection tools, and credit bureau services.

An API-first architecture like we have in ServoStreams powered Loan origination solutions ensures data flows in real time. Moreover, credit bureau reports should be fetched instantly. Fraud checks should run automatically. Disbursement should trigger without manual duplication of effort.

When systems communicate smoothly,your teams work more efficiently and your customers experience fewer delays.

4. Risk Analytics That Give You Strategic Visibility

As your lending portfolio grows, visibility becomes critical.

Your LOS should provide real-time dashboards that track approval ratios, turnaround time (TAT), portfolio segmentation, underwriting productivity, and emerging risk indicators. These insights help you identify bottlenecks early, adjust credit policies proactively, and monitor portfolio health continuously.

Instead of reacting to issues after they escalate, you gain the ability to make informed decisions based on live operational data.

5. Built-In Compliance and Security Controls

Your Loan Origination System must embed compliance and security into its foundation. Sensitive borrower data should be encrypted. Role-based access should ensure controlled visibility. Every action within the system should be logged for audit readiness.

When regulators request documentation or review processes, you should be able to respond with confidence — backed by structured audit trails and transparent workflows. Remember, security and compliance should not feel like separate tasks. They should be seamlessly integrated into your daily operations.

How to Implement a Loan Origination System

Successful LOS implementation is not just about installing software. It is about carefully aligning technology with your lending processes, risk framework, and compliance obligations. A phased approach ensures smoother adoption and long-term success.

Step 1: Process Mapping

Begin by documenting your existing loan workflows in detail.

Map how applications move from intake to disbursement. Identify approval layers, verification checkpoints, exception handling processes, and manual bottlenecks. This step helps you clearly understand where delays, redundancies, or risk gaps currently exist.

Without this clarity, automation may replicate inefficiencies instead of eliminating them.

Step 2: Policy Digitization

Next, translate your credit policies into system-driven rules.

Eligibility criteria, risk scoring logic, debt-to-income thresholds, pricing guidelines, and escalation triggers should be embedded into the rule engine. This ensures consistent underwriting decisions across branches, products, and teams.

Digitizing policies reduces subjectivity and strengthens governance by making every decision traceable to a predefined rule.

Step 3: Workflow Configuration

Design your approval hierarchies and escalation logic within the system.

Define role-based access controls for credit analysts, risk managers, and committees. Establish maker-checker mechanisms. Configure exception workflows for cases that fall outside standard parameters.

This step ensures accountability, transparency, and controlled decision-making across your organization.

Step 4: Bureau and API Integration

Integrate the LOS with your broader ecosystem.

Connect with credit bureaus for real-time data retrieval. Link your Core Banking System (CBS) for seamless disbursement. Integrate fraud detection tools, CRM systems, and payment gateways as needed.

An API-driven architecture eliminates data silos and ensures smooth information flow across platforms.

Step 5: Pilot Deployment

Before a full rollout, test the system in a controlled environment.

Select specific branches, products, or teams to run pilot cases. Monitor system behavior, workflow efficiency, and user adoption. Identify configuration gaps and fine-tune processes.

This phase reduces risk and builds confidence before scaling.

Step 6: Regulatory Validation

Validate that the system aligns with regulatory and compliance requirements.

Ensure audit trails are active. Verify documentation controls. Confirm reporting capabilities meet internal and external regulatory standards.

Regulatory readiness should be built into the system — not addressed after deployment.

Step 7: Full-Scale Rollout

Once validated, move toward organization-wide deployment.

Train teams across credit, operations, and risk functions. Establish clear performance metrics such as turnaround time (TAT), approval ratios, and exception rates. Continuously monitor KPIs to measure impact and optimize performance.

Implementation does not end at go-live. Ongoing monitoring ensures the system continues to deliver operational efficiency and risk control as your lending portfolio grows.

Loan Origination Implementation Mistakes You should Avoid....

Implementing a Loan Origination System is not just a technology deployment — it is an operational transformation. Many projects underperform not because the platform is weak, but because foundational planning gaps create friction during rollout. Here are the most common mistakes institutions make:

• Over-customization

Excessive customization to mirror legacy processes often increases cost, delays deployment, and makes future upgrades difficult. Instead of redesigning workflows for efficiency, institutions sometimes digitize inefficiencies. A configurable, policy-driven approach works better than heavy code-level modifications.

• Ignoring Integration Complexity

An LOS must integrate with core banking systems, credit bureaus, KYC providers, payment gateways, fraud tools, and CRM platforms. Underestimating API architecture, data mapping, and middleware requirements can cause major delays and operational instability post-launch.

• Poor Change Management

Technology adoption fails when teams are not aligned. Credit officers, operations staff, risk managers, and branch teams must understand new workflows. Without structured training, internal communication, and leadership advocacy, resistance slows ROI realization.

• Inadequate Data Migration Planning

Migrating historical loan files, customer records, and document archives requires careful validation, cleansing, and indexing. Poor migration strategy can lead to missing data, broken linkages, and audit exposure.

• Lack of Executive Sponsorship

LOS implementation impacts risk governance, compliance, IT, and operations. Without strong executive ownership, cross-functional alignment weakens and decision-making slows — jeopardizing timelines and outcomes.

Structured planning, phased deployment, stakeholder alignment, and integration readiness significantly reduce these risks — ensuring the Loan Origination System delivers measurable business impact rather than operational disruption.

The Future: AI-Powered Loan Origination

Digital transformation in lending is no longer about moving applications online. It is about making decisions smarter.

AI powered loan origination goes beyond static workflows and basic rule engines. It brings predictive risk modeling, behavioral scoring, anomaly detection, and adaptive decision systems that learn from portfolio performance over time. Instead of reacting after stress appears, institutions can identify early warning signals. Instead of manually reviewing every exception, systems can prioritize risk dynamically and consistently.

For banks and NBFCs operating under strict regulatory oversight, this intelligence must remain governed and explainable. AI should reinforce credit policy — not override it. The real advantage lies in combining automation with analytics, speed with compliance, and innovation with control.

This is where Servosys Loan Workflows align with the future of digital lending. Built on a configurable, API-driven architecture, Servosys enables institutions to embed AI-powered underwriting, structured rule engines, compliance validation, and real-time risk visibility into a single orchestrated framework. The outcome is not just faster approvals, but standardized, auditable, and scalable credit decisioning.

Because the future of lending is not just digital. It is structured, intelligent, and AI powered.

FAQs

FAQs on Loan Origination System

What is the difference between a Loan Origination System (LOS) and a Loan Management System (LMS)?

A Loan Origination System manages the pre-disbursement process (application to approval). A Loan Management System (LMS) handles post-disbursement activities such as EMI tracking, repayments, collections, and portfolio monitoring.

What features should banks look for in loan origination software?

Banks should prioritize workflow automation, rule and decision engines, credit bureau integration, API-based architecture, compliance controls, audit trails, analytics dashboards, and cloud scalability.

How does a rule engine improve credit governance?

A rule engine enforces predefined credit policies automatically. It applies eligibility criteria, risk thresholds, and escalation logic consistently, reducing underwriting subjectivity and strengthening governance.

Can a Loan Origination System integrate with Core Banking Systems?

Yes. Modern LOS platforms use API-based integration to connect with Core Banking Systems (CBS), credit bureaus, KYC services, CRM tools, fraud detection systems, and payment gateways for seamless data flow.

How long does LOS implementation take?

Implementation timelines vary based on integration scope, product complexity, and regulatory requirements. A phased rollout approach — including pilot deployment and compliance validation — reduces risk and accelerates adoption.

Can an LOS support multiple loan products?

Yes. A configurable loan origination system can support retail loans, SME lending, corporate credit, housing finance, and microfinance — each with product-specific workflows and approval hierarchies.

Transform your Lending Journeys!

Innovate, simplify, and expand with cutting-edge process automation solution.

- Gold Loan

- Consumer Durable

- Home Loan

- Microfinance

- MSME Loan

- Education Loan

- Construction Finance

- Corporate Loan

- Personal Finance

- Vehicle Loan